As an American, your credit score affects many aspects of life, such as your ability to open a credit card and bank account. It can also impact bigger life decisions, such as buying a home and car or getting a loan with a good interest rate.

If you’ve painstakingly built your credit score stateside, you might wonder whether other countries have credit scores and if your credit will follow you should you decide to relocate. The answer to this is no; your credit score is not international, and it does not transfer to other countries. Credit scores in other countries are calculated using their own scoring systems, so you’ll need to establish a new credit history in that country.

Read on to learn more about what countries use credit scores and whether your U.S. creditworthiness holds any weight internationally.

KEY TAKEAWAYS

- Your U.S. credit score does not follow you to other countries.

- Countries have their own credit scoring systems, though the systems in Canada, the U.K., and Mexico are most similar to American scoring models.

- When you relocate from the U.S. to another country, you’ll have to rebuild your credit history according to the country’s system.

- Generally speaking, factors such as debt levels and income are used to determine creditworthiness internationally.

Understanding the U.S. Credit System

In the U.S., your three-digit credit score is used to help lenders determine your creditworthiness — that is, how likely you are to repay a loan over time. Lenders will report your payment history to one of the three major credit bureaus, Experian, Equifax, or TransUnion, and then credit scoring companies like FICO or VantageScore will use that data to generate your credit score.

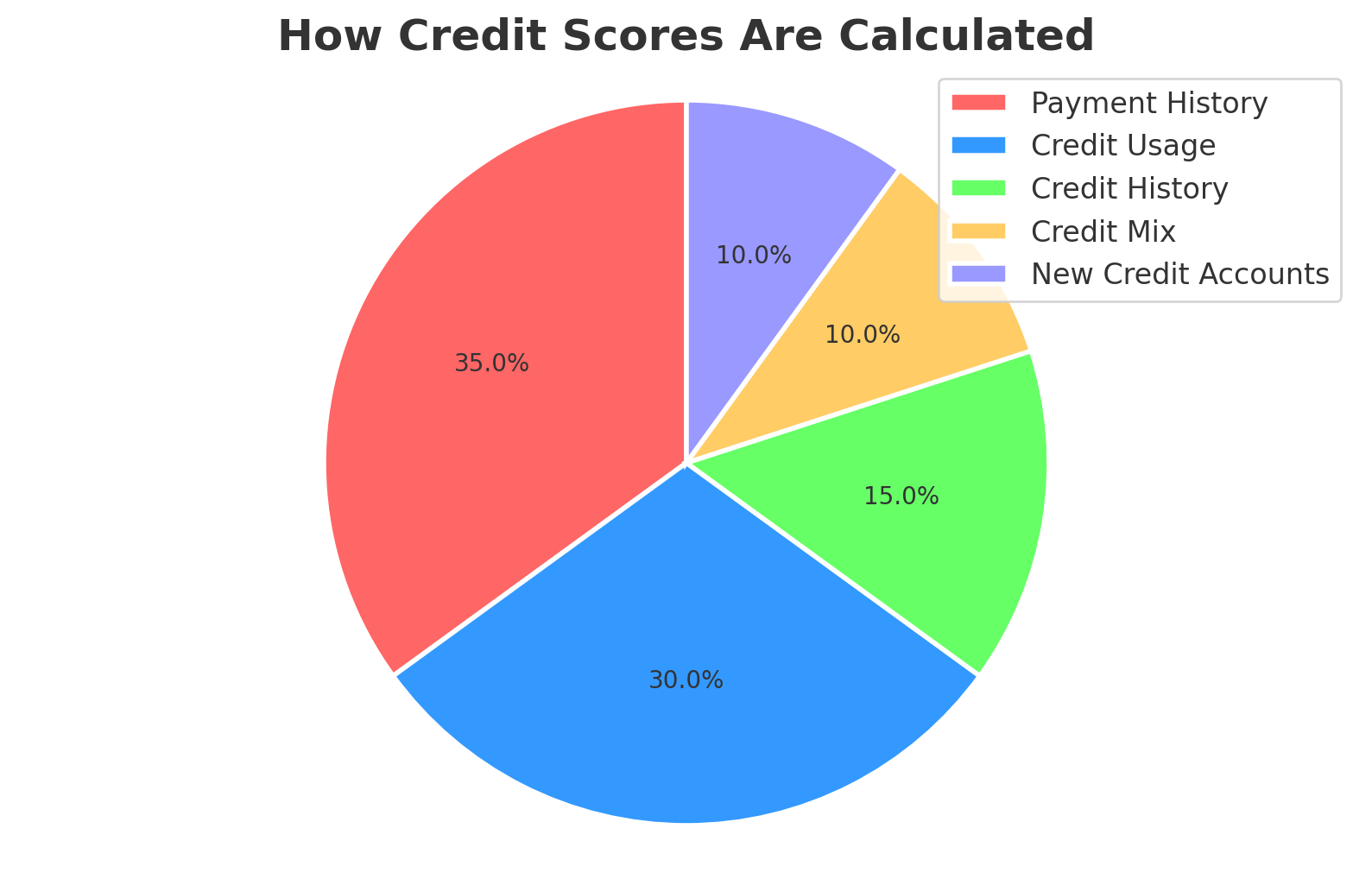

Credit scores in America fall between 300 and 850. It is calculated largely based on your payment history, but institutions also consider several other factors to gauge your creditworthiness:

- Payment history: whether you pay your bills on time

- Credit usage: what amount you owe and how much of your available credit you use

- Credit mix: total number of accounts you have like: mortgages, loans, credit cards

- New credit accounts: how many new accounts you open

- Credit history: how long your credit history spans

Here is a pie chart, where major categories are grouped, showing how credit scores are calculated:

Lenders use your credit score to decide whether to offer you a loan, credit card, or other financial product, and by extension, the loan terms and rates associated with it. Higher scores usually translate to better approval odds and terms, and lower scores usually warrant lesser odds because you are seen as a higher risk.

Credit scores of 700 and above are generally considered good; however, every creditor has their own guidelines for categorizing them. Here’s a general guide:

- Poor: 300–580

- Fair: 580–669

- Good: 670–739

- Very Good: 740–799

- Exceptional: 800–850

In America, you can increase your credit scores by paying off your bills on time, not closing your credit card accounts arbitrarily, and making better financial decisions. Credit scores in other countries are determined by different scoring systems, and you’ll need to understand how they calculate them before building an international credit history.

Does Your Credit Score Transfer to Another Country?

Other countries have credit scores, but your credit score does not follow you to other countries. There are no international credit scores, and data protection laws do not allow countries to share credit information overseas.

For example, credit scoring systems in Canada and the U.K. are similar to the American system but they do not communicate with eachother. Japan has no formal credit system and relies on information like your relationship with the bank to determine creditworthiness.

That said, a history of responsible financial decisions — on-time payments, low credit utilization, and proof of income — will serve you well in every country.

What Countries Use Credit Scores and How Do They Work?

In this section, we’ll discuss what countries have credit scores and explain the unique features of credit scoring systems in Europe, Asia, and other international destinations.

Credit Scores in Canada

Canada’s credit scoring system is most similar to the one used in America. The score is calculated by Canada’s two main credit bureaus, Equifax and TransUnion. Resident scores can range from 300 to 900 based on your credit history, how much credit you use, payment history, and public records.

In Canada, a good credit score is between 740 and 799, while anything above 800 is excellent. You can get a free credit report for Canada with Equifax or TransUnion.

Credit Scores in the United Kingdom

The credit score rating system in the United Kingdom isn’t too different from the U.S. and Canadian systems. Residents of the U.K. are assigned a three-digit number based on calculations from the country’s three main credit reference agencies (CRAs): Experian, Equifax, and TransUnion. While each CRA has a varied definition of what a great credit score in the U.K. looks like, the main determining factors include repayment history and credit limit to credit utilization ratio.

Agencies in the U.K. are unique in that your credit score will also consider whether you’re registered to vote when determining your score, which is verified using the electoral roll. The table below provides a credit score breakdown in the U.K., according to the three CRAs:

| Credit Score | TransUnion | Equifax | Experian |

|---|---|---|---|

| Excellent | 628–710 | 466–700 | 961–999 |

| Good | 604–627 | 420–465 | 881–960 |

| Poor | 566–603 | 380–419 | 721–880 |

Credit Scores in China

The Chinese social credit system takes a more holistic approach to credit ranking by considering an individual’s actions in society. This rating strategy is still in development, but it uses a mixture of financial stability and social factors like hard work, devotion to family, honesty, traffic violations, and arrest warrants in determining one’s eligibility for credit.

A person with a poor social credit score in China may struggle to get a job, access loans, and secure approval to travel overseas.

Credit Scores in Japan

Does Japan have credit scores? No, Japan does not operate any formal credit scoring system. Instead, individuals access loans based on their relationship with their banks. For banks to make decisions on loans, they will individually consider employment history, outstanding debts, and availability of collateral.

Credit Scores in Norway

Norway is home to three credit reporting agencies: Dun & Bradstreet, Experian, and Lindorff Decision. Depending on the reporting agency, your score can range from 1 to 100 or 1 to 1,000. Instead of a traditional three-digit number, Norway uses a detailed report known as a credit score assessment. The higher the score, the higher the chances of getting a loan and favorable terms and interest rates.

The credit score is based on available information about your debt-to-income ratio, assets derived from your yearly tax return, and demographic data such as your age and address. Any negative payment behavior, called “betalingsanmerkning” in Norwegian, will also be considered and negatively affect the credit score.

Credit Scores in Australia

Your credit score in Australia is a number between zero and 1,000 or 1,200, depending on the credit reporting agencies. The three main agencies are Equifax, Experian, and Illion. Scores above 700 are considered very good, determined by your payment and credit history, debts owed, credit mix, and negative reports.

Previously, Australia only reported negative marks in credit scores but transitioned to a more comprehensive financial picture in 2024.

Credit scores are not international, meaning they do not transfer to other countries. However, the country you move to likely has its own credit ranking system that will determine your ability to apply for loans and credit. It’s important to develop good financial habits and pay your bills on time.

FAQ

Below, we’ve answered some common questions about credit scores in other countries.

How Can I Build Credit Abroad?

Building credit in another country requires good financial habits, such as paying your bills on time and keeping your credit utilization low. Open a bank account as soon as you arrive, and if possible, apply for a secured credit card to start establishing a local credit history. It’s also important to maintain your U.S. credit score while abroad by continuing to pay your U.S. debts on time, especially if you plan to move back in the future and apply for loans.

Does Your Credit Score Follow You to Another Country?

No, your credit doesn’t follow you to another country. But relocating somewhere outside U.S. borders won’t erase your existing loans or debt and your responsibility to pay them. The lender might also sell the debt to a collector. If your debts are in collections, debt collectors will continue contacting you about a repayment plan and, eventually, a lawsuit to collect the debts if they can’t reach you. Such actions will negatively affect your credit score and reduce your financing options when you return to the U.S.

Are Credit Scores International?

If you’re wondering, “Do other countries have credit scores?” the answer is yes. While other countries outside the United States have credit scores, there is no internationally recognized credit rating system, and their scoring systems differ. Countries such as Japan, Spain, France, and the Netherlands don’t use credit scores to determine creditworthiness but may use other methods, like blacklists, to track individuals who fail to repay loans.

Does Europe Have Credit Scores?

There are no generally accepted credit score systems across Europe. Some countries, like Germany and the U.K., have credit rating systems that consider factors like the borrower’s savings, income, repayment history, and length of employment to determine credit score.

Then there are countries that don’t have a full-fledged credit scoring system but have some form of credit register for debtors. For example, Austria and Sweden use a blacklist system to track those who fail to pay bills. Italy has a Central Credit Register managed by the Bank of Italy that keeps records of debtors. Switzerland’s credit scoring system uses an income-to-expenses ratio to determine creditworthiness.

Does Your Credit Score Follow You to Another State?

Credit scores are nationally recognized in all U.S. states, so your score will stay the same no matter where you live. Changing your address or relocating to another state can impact your credit score if it means that you apply for a mortgage loan or other financial product that requires a hard credit check.